November 17, 2023

Last Updated

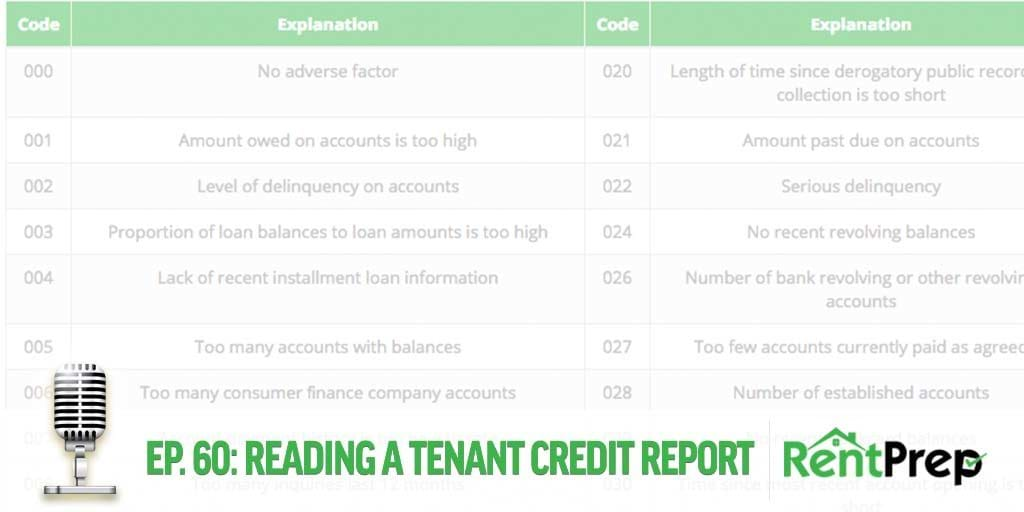

A tenant credit report is a very important part of tenant screening but many people are unclear about the different inquiry types. In this episode of Night School, we’ll explain the inquiry types on a credit report and exactly what landlords need to know about them.

Transcription from Inquiry Types on a Tenant Credit Report

Jeff: Welcome to Landlord University Night School. I’m Jeff Pearson and this is my co-host…

Stephen: Stephen White.

Jeff: Hello Stephen, how are you this evening?

Stephen: Pretty good, Jeff. We’ve got an interesting topic. We talked about it a lot with landlords. We talk about it a lot with tenants who call us and have questions about their credit. And so, we’re going to be talking about inquiry types. Different types of credit inquiries that can show up and appear on a person’s or your own credit report. So there’s two different types of inquiries. There is a hard inquiry and a soft inquiry. And just to identify the different types first. The hard inquiry, this is if you’ve ever filled out an application for, you know, credit. If you have, you know, applied for a car loan, a credit card, tenant’s screening. So if you’re applying for an apartment, a mortgage, anything like that, anything that you’ve given written authorization to pull your credit. That is considered a hard inquiry.

A soft inquiry is any time that somebody pulls your credit usually without your knowledge or you’re pulling your own credit. So a case where somebody will pull your credit without your knowledge would be if you’ve ever gotten in the mail, a million of those preapproved mortgage, you know, letters or preapproved credit cards. They are basically scanning hundreds of thousands of credit reports looking for the right criteria. You know if your credit score is over a certain number or whatever the case is, they’re gonna give you this preapproved offer base on your credit. They don’t need permission, believe it or not, to pull your credit on those cases. But they’re not pulling your full credit report, so it’s considered just a soft inquiry.

A common misconception is that hard inquiries regardless of where they’re coming from or the types that they are, are going to impact your credit negatively, which is not true. So if I were to, you know, let’s assume that I’m somebody with good credit, if I were to go and get a car, just because I went and applied to get a car and applied for credit, doesn’t mean that I’m going to have bad credit after I do that. People with good credit apply for credit all the time and it doesn’t affect their credit. So, there’s, you know, there’s a reason behind inquiries that hurt your credit and why they would hurt your credit.

Jeff: So if you went to a dealership to apply for credit to get a car and you were turned down, then you went to another dealership to apply and you got turned down. And you repeated that two, three, four times, then it would…it possibly would start to affect your credit. But one time, no big deal.

Stephen: Well, that absolutely is gonna affect your credit. What it is that actually triggers a negative effect in your credit is the number of inquiries. And there’s an actual code for it in, you know, in the credit reporting algorithm and the credit score algorithm and how they calculate this stuff. So, it is the number of inquiries in the past 12 months that’s going to affect your credit. And what they’re looking for, you know, understandably so, they’re looking for people who are just going out try to gobble up as much available credit as possible. That’s obviously not good for you. It’s not good for other creditors who are looking to lend to you. They wanna be sure that, you know, like you just said you didn’t go to three other dealerships and got turned down, and you’re just gonna continue to go and do it over and over and over. So in those cases, it will impact your credit negatively. It will start to drag the score down. They see you as somebody who’s, again, just going out trying to get as much credit as possible and especially when they see that that inquiry doesn’t convert into a trade line. In other words, you were denied the credit. So, if they see Ford Motor credit as an inquiry and then, a month later Ford Motor credit still doesn’t show up as a trade line. In other words, you have no account with them. They know that that was just a pull and you were denied credit.

Jeff: Right.

Stephen: So that’s going to, you know, have a worse, long-term than if you’re treating your credit carefully, you’re only applying to things that are useful, meaningful, whatever, you know however you want to word it. But you’re not just being, you know, too loose with it. It’s gonna have no negative impact, long-term negative impact on your credit. If I were to go out right now and apply for credit, it may impact my score by a point or two for a day or two, but it’s going to come right back up. So, you know, it depends on who the person is and how that’s going to affect their credit and certainly their credit history is going to have the biggest impact on that.

Jeff: So if somebody is trying to rent a property and they go out and apply at three or four different properties, and each of those prospective landlords does a credit check. Then that’s going to have some negative impact on someone’s credit score.

Stephen: It could potentially, depending on their credit situation going into it. And again, you know, the most obvious question is going to be, you know, and from the perspective of the credit bureaus is, “Why did you need to apply to three different places?” So, you know, assuming that you were getting turned down is what they’re going to make the assumption of is that, “Okay. They’re going out there, you know, in a week’s span here, they’ve applied to three different places or…” you know. And again, it’s all considered into what’s happened before that too. If you’ve got 10 other inquiries on there for department store credit cards or, you know, cell phone companies or whatever the case is, again, it doesn’t look good. It doesn’t look like somebody who’s, you know, financially responsible. And ultimately, that’s what, you know, these algorithms are trying to determine by giving you a score, is what is your level of creditworthiness? How financially responsible are you really?

Jeff: And if you have a good credit score and a good credit history, it’s not that big a deal. If it’s, you know, if you’re really trying to get it higher even if it’s a decent score and you’re trying to make it higher, I can think around here in the San Francisco Bay area, there are places that come up for rent and you have 10, 20, 30 people applying for a rental. And I’m sure the prospective landlords are not running background checks on all of those people, but if you happen to be somebody who ends up in the top three or the top five and you keep getting turned down just because there are a number of other people applying for the same property, you could go through a number of different processes before you get to the one that you finally rent. And it could take two, three, four, five different applications to finally get a rental property.

Stephen: Yeah, definitely. And I think in those cases for sure it’s definitely important for the tenant to make mention of it. I think that any time that a tenant goes into a situation with full disclosure, you know, whether you have an eviction on your record, a criminal record, whether your credit’s bad, if your credit’s bad and you’re a tenant and you approach the landlord and say, “Listen, here’s the background story,” you know, and or, “Here’s the reason why,” or, you know, “This…just to let you know, this happened but now I’m in good standing,” or whatever. If they’re legitimate, you know, and they’re serious about it, it’s definitely a really common call that we get here at RentPrep a lot is a landlord will call and say, “Hey, this guy told me he’s got some bad credit issues.” You know, or, “This guy told me that, you know, he was evicted three years ago, and since then he’s good.”

So, what they’re gonna be looking for is, you know, they’re willing to consider that noted. I mean, the element of surprise is the worst thing when you’re looking at background checks. So, if you know it going into it, you’re a lot less likely to count that against them negatively. So, the different types of inquiries, you know, we’ll get a lot of tenants that will ask too, you know, “Well, what kind of inquiry is this gonna be on credit?” And it’s a legitimate question. I mean, they want to know, you know, is it going to affect them negatively. So, for pulling credit, yes, it could potentially affect them negatively. If you’re just doing a background check, which includes, you know, anything other than credit reports, so if you’re looking at bankruptcies, judgments, liens, evictions, criminal history, any of those types of things, none of those things generate an inquiry on a credit report. So, it’s also important to know if you had somebody that that’s a concern and you still considering them, you don’t necessarily have to pull the full credit report on them.

Jeff: Get the background check first. Make sure that everything is good there. And then if it is somebody that you want to consider, then you could do the credit report.

Stephen: Yeah. You know what I always told landlords that’s the best way to go anyway. If you’re gonna do a background check on somebody and you find out that they’re in the process of getting evicted, their score does not matter to you, you know, their credit doesn’t matter at all. Or, if you find out that they are a sex offender or they got a history of violent crime or whatever the case is, at some point that credit score is just totally irrelevant to you. It doesn’t matter at all. So the background check is just as important and can certainly be done in order too.

So, different types of credit inquiries is definitely important for landlords to understand the different type just in case they come across the question. And the other important thing to note is, you know, we’ve talked about the importance of good record keeping for a landlord. You have to keep on file, for a minimum of five years, that rental application that that, you know, perspective tenant had signed giving you authorization to pull their credit. Because if they ever do dispute it and they run it through the credit bureaus, you have to have proof, you have to have proof that they had given authorization to do so.

So, that’s the best example that I can give of why you would need to keep a good record of…especially a rental application even if you denied them, you know. Don’t toss is in the garbage just because they didn’t get the apartment. You got to hang onto it. It’s part of your landlord duties of good record keeping. You got to hang onto those. And just look at it as, you know, in the event that something ever does come up, you’ve got that proof, that written consent that you were given authorization to view their records.

Jeff: Yes. And that is the type of document that you would want to scan and upload. We were just talking in the last episode about storing things in the cloud. Make sure that you keep a copy of that away from your house. And scan it, upload it to Dropbox or Google Drive or something. So that you have access to it and you have a backup copy of it as well.

Stephen: Definitely, yeah. Good advice too is when you’re saving these type of things obviously, you got to save it where it’s secure. So security is paramount. Save them with the initials of the person or first name, last initial, or first initial, last name. You don’t want to put the two combinations together. Any time that you can avoid that you want to. But you want to have the ability to be able to search for those items. So if you have, you know, 100 or 200 applications instead of having to sift through them all and dig through them, you have the ability to just type in Jeff P. and pull up anybody with Jeff P. that has an application in there.

Saving them with the name or saving them with the address, you know, an indication there, if you’ve got a lot of properties, it’s another great way to store documents so you can search things by a specific address.

Jeff: Sounds good. Well, great. Stephen, I think that wraps up another episode of Night School. I’ll look forward to talk with you tomorrow.

Stephen: Right. Thanks Jeff.